There is a moment in every great technological transition when it stops being a story about software and starts being a story about the physical world. On the topic of AI – and the investment being poured into the infrastructure to support its transformational development – we are entering that moment now.

Whether you believe AI is a bubble or not, this investment is real. Much like the early days of the dot.com boom, and the necessary investment in creating the plumbing to support the web, this wave of AI investment will change the way we live beyond simply being an investment story.

Recently, several developments have pointed in the same direction. AI is no longer primarily about models and applications – it is about power and long-duration capital commitments.

Recent Large-Scale Investments

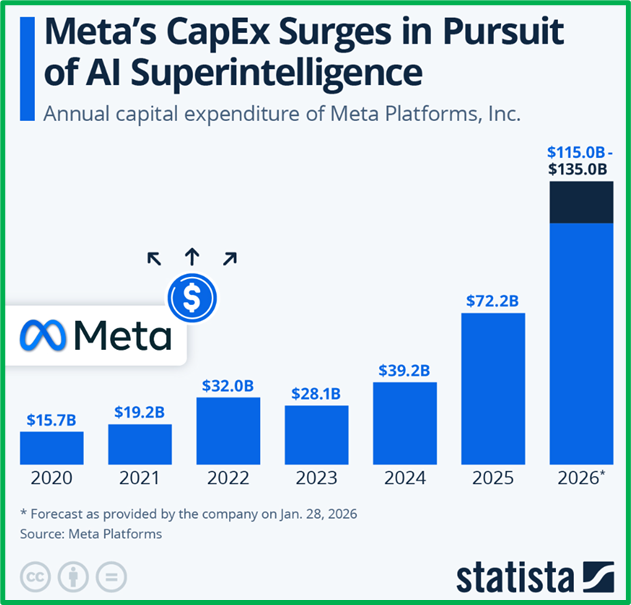

Meta Platforms announced an expanded multi-year partnership with Broadcom to develop custom AI accelerators, including next-generation chips on advanced process nodes. The companies outlined an initial deployment measured in gigawatts of compute capacity, with a roadmap extending through the end of the decade. That is not a product launch cycle. It is infrastructure planning.

At the same time, CoreWeave and Meta disclosed a long-term cloud capacity agreement worth approximately $21 billion through 2032. Combined with a previously announced $14.2 billion arrangement, total contracted value between the two companies now exceeds $35 billion. These are not exploratory budgets or software companies updating their terms of service. This is concrete, capital-intensive infrastructure being financed, built, and locked in years in advance.

The earnings are not lying

In investing, a supercycle refers to an unusually long and powerful period of growth in a particular asset class, sector, or the broader economy—lasting much longer than a typical business cycle. The supercycle in AI arguments live or die on whether the underlying demand is real.

The earnings season just provided a compelling answer. TSMC reported a 58% jump in first-quarter profits, hitting a record and extending its streak of double-digit profit growth to eight consecutive quarters, and guided for full-year revenue growth exceeding 30%. ASML, the only company on earth capable of making the extreme ultraviolet lithography machines needed to produce advanced chips, raised its 2026 revenue outlook to between €36 billion and €40 billion, with its CEO noting that demand for chips is outpacing supply. These are not speculative growth companies describing future pipelines; they are the essential picks-and-shovels of the AI age reporting actual revenue.

Further down the stack, India’s Tata Consultancy Services crossed $2.3 billion in annualised AI revenue in the latest quarter, with clients graduating from experimentation to large-scale, multi-year commitments. Sustained infrastructure buildouts require demand from both the hyperscalers investing at the frontier and the enterprises deploying at scale. Both signals are now present.

When energy policy bends to compute

The most striking indicator that this is structural rather than cyclical may not be found in any earnings report. It is found in the fact that AI is now powerful enough to reverse energy policy decisions that took decades to establish.

Taiwan’s President has signalled openness to restarting two decommissioned nuclear plants to meet the power demands of the AI and semiconductor industries, a remarkable shift for a government that built its political identity around a nuclear-free homeland pledge.

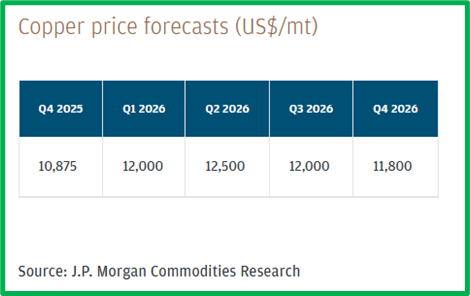

In the United States, multiple hyperscalers have signed contracts for small modular reactors. Uranium spot prices, volatile as they are, have structurally repriced upward from the lows of recent years. Copper futures are approaching $6.1 per pound, driven partly by the reality that a modern AI data centre can require up to ten times the electrical load of a conventional facility.

JPMorgan projects a global refined copper deficit of around 330,000 tonnes in 2026, with AI data centre installations alone consuming an estimated 475,000 tonnes. The commodity complex is pricing a multi-decade buildout.

Not all birds will fly

A structural shift does not imply universal success. In fact, history suggests the opposite. The existence of a genuine supercycle does not mean that every company wearing an AI badge will survive it. History is unambiguous on this point.

The railroad boom of the 19th century was real, and it bankrupted the majority of the companies that built the railroads. The internet revolution was real, and it destroyed more capital than it created in its first decade.

This week delivered a perfect parable. Allbirds, the once-beloved sustainable sneaker brand that became a symbol of Silicon Valley’s eco-conscious moment, announced it was pivoting from wool shoes to AI compute infrastructure, rebranding itself “NewBird AI.” The stock surged 582% in a single session. By the following morning, it had fallen 36%. The company had sold its entire footwear business for $39 million just weeks earlier, after being valued at $4 billion at its 2021 IPO. It was a masterclass in the distinction between a theme and a business.

The real winners of this buildout are visible and, by and large, already well-capitalised. Nvidia has constructed an ecosystem moat that extends beyond chips into software, interconnects, and now strategic equity stakes. TSMC has manufacturing advantages that cannot be replicated in years.

The hyperscalers, Meta, Google, Amazon and Microsoft, are both customers and architects of the infrastructure layer, with balance sheets that allow them to commit billions over multi-year horizons. CoreWeave has demonstrated that there is a lucrative middle layer to be built between chip manufacturers and end users. These companies are not pivoting to AI. They are AI.

Why this time is different

The dot-com era had vision but it lacked physical constraint and was defined by low barriers to entry. You could incorporate a company, buy a domain, and raise hundreds of millions of dollars without building anything physical. The AI supercycle is different in kind. Long-term contracts are being signed between companies whose CFOs are not known for sentimentality.

The world is not at peace. Geopolitical risk is elevated, energy markets are volatile, and recession risks are non-trivial. But the capital flowing into AI infrastructure is not moving because of optimism about the next quarter. It is flowing because the companies deploying it believe that compute is the defining scarce resource of the next decade, and that the cost of being under-invested dwarfs the cost of being wrong.

None of this eliminates the possibility of overbuild or misallocation of capital. After all, infrastructure cycles often overshoot and end with massive overcapacity. Pricing for AI services may compress as competition increases. Macroeconomic conditions could still constrain demand. Even with those caveats, something important appears to be changing.

Taken all together, these signals suggest that AI is no longer just a software narrative. It is increasingly a story about infrastructure that is expensive, physical, and difficult to build. Although AI has a very low barrier to entry at the application layer, it has a very high barrier to entry at the infrastructure layer. AI is not a low-barrier technological wave like the early internet. The consequence of this is fewer winners at the infrastructure level, but still a lot of noise, competition and churn at the application level.

The AI infrastructure boom will go on.

IFA Magazine – 14 May 2026

Why AI is becoming an infrastructure supercycle, not a tech story – IFA Magazine