Quote – “There are known knowns; there are things we know that we know. There are known unknowns; things we know we don’t know. And there are unknown unknowns; things we don’t know we don’t know.” Donald Rumsfeld

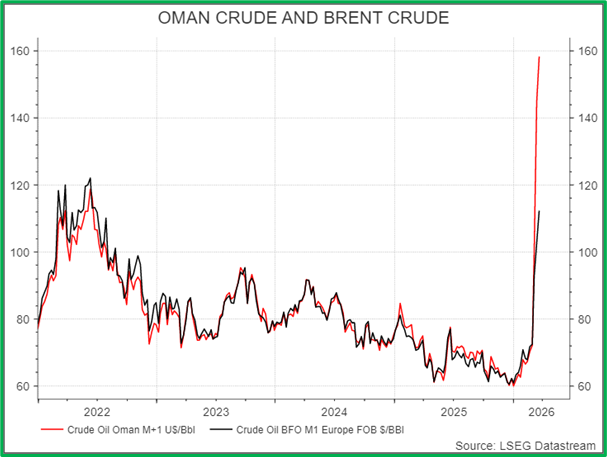

The recent escalation in the Middle East has evolved beyond a regional conflict and now represents a significant global macroeconomic shock. Developments in recent weeks, including the effective closure of the Strait of Hormuz and strikes on critical LNG infrastructure, illustrate how rapidly geopolitical events can transmit into the global economy. While the situation remains fluid, most investment portfolios are being affected, albeit to differing degrees depending on underlying exposures.

The current environment is being shaped by a combination of forces: rising energy prices, disruption to global shipping routes, renewed inflationary pressure as well as the prospect of a lower growth environment. Together, these dynamics are contributing to a more uncertain and fragile market backdrop.

From a current portfolio perspective, the present challenges are firstly in determining what the most likely core scenario will become moving forward in such a fast moving and uncertain environment, as well as a lack of sufficiently stable conditions in which to act with conviction. In periods such as this, discipline is best maintained not through activity, but through planning and patience.

In framing this outlook, three broad scenarios remain relevant:

- Continuation of the current level of conflict

The situation persists at its current intensity, with ongoing but contained disruption to energy flows, particularly in key by-products such as jet kerosene. Inflation remains persistent, growth slows, and central banks maintain a cautious stance. Markets continue to exhibit elevated volatility and sensitivity to news flow. This scenario makes rebalancing model portfolios particularly challenging, as the risk of being whipsawed is significantly elevated. In this environment, the prudent approach is to continually assess the situation and wait for clear signs that the conflict is evolving into one of the two scenarios below, which would provide an opportunity to take action.

- Escalation

If the conflict broadens further, leading to more severe and sustained disruption to energy supplies, inflationary pressures will intensify and downside risks to growth will increase. Policy trade-offs become more complex and market volatility rises, with greater pressure on risk assets. Should this become the core scenario, a risk management rebalance may be required to reposition portfolios for a significant deterioration in both the economic and market outlook.

3. De-escalation and stabilisation

Finally, there exists the possibility that tensions ease and energy markets begin to normalise. Inflationary fears might moderate, and growth expectations stabilise, allowing central banks to regain greater flexibility. Market conditions improve, supporting a broader recovery in risk assets.

Across all scenarios, portfolios should be continually evaluated, and one must be prepared to adjust portfolio(s) positioning as conditions evolve. The key consideration at present is timing rather than direction.

The latest market reactions reinforce the importance of this approach. A single, unconfirmed development has been sufficient to drive meaningful asset price movements, despite no substantive change in underlying risks. This serves as a reminder of the importance of distinguishing between short-term noise and more durable shifts in the macroeconomic environment.

Why is this so important?

We continue to monitor developments closely, including geopolitical signals, market pricing, and our internal indicators. Greater clarity, particularly around the duration and extent of disruption in energy markets, is required before implementing any material portfolio changes.

Until such clarity emerges, our focus remains on maintaining discipline, preserving optionality, and ensuring that when conditions do stabilise, we are well positioned to act decisively and in alignment with long-term objectives.

Disclaimer: FOR PROFESSIONAL USE ONLY. This report was produced by Collidr Research (“Collidr”). The information contained in this report is for informational purposes only and should not be construed as a solicitation or offer, or recommendation to acquire or dispose of any investment. While Collidr uses reasonable efforts to obtain information from sources which it believes to be reliable, Collidr makes no representation that the information or opinions contained in this report are accurate, reliable or complete. The information and opinions contained in this report are provided by Collidr for professional clients only and are subject to change without notice. You must in any event conduct your own due diligence and investigations rather than relying on any of the information in the report. All figures shown are bid to bid, with income reinvested. As model returns are calculated using the oldest possible share class, based on a monthly rebalancing frequency and all income being reinvested, real portfolio performance may vary from model performance. Portfolio performance histories incorporate longest share class histories but are either removed or substituted to ensure the integrity of the performance profile is met. The value of investments and the income from them can go down as well as up and past performance is not a guide to the future performance.

Collidr Research is a trading name of Collidr Technologies Ltd, registered in England and Wales No. 09061794. Registered office: Adler House, 35 36 Eagle Street, London, WC1R 4AQ.