‘Things are not always what they seem’ – Plato

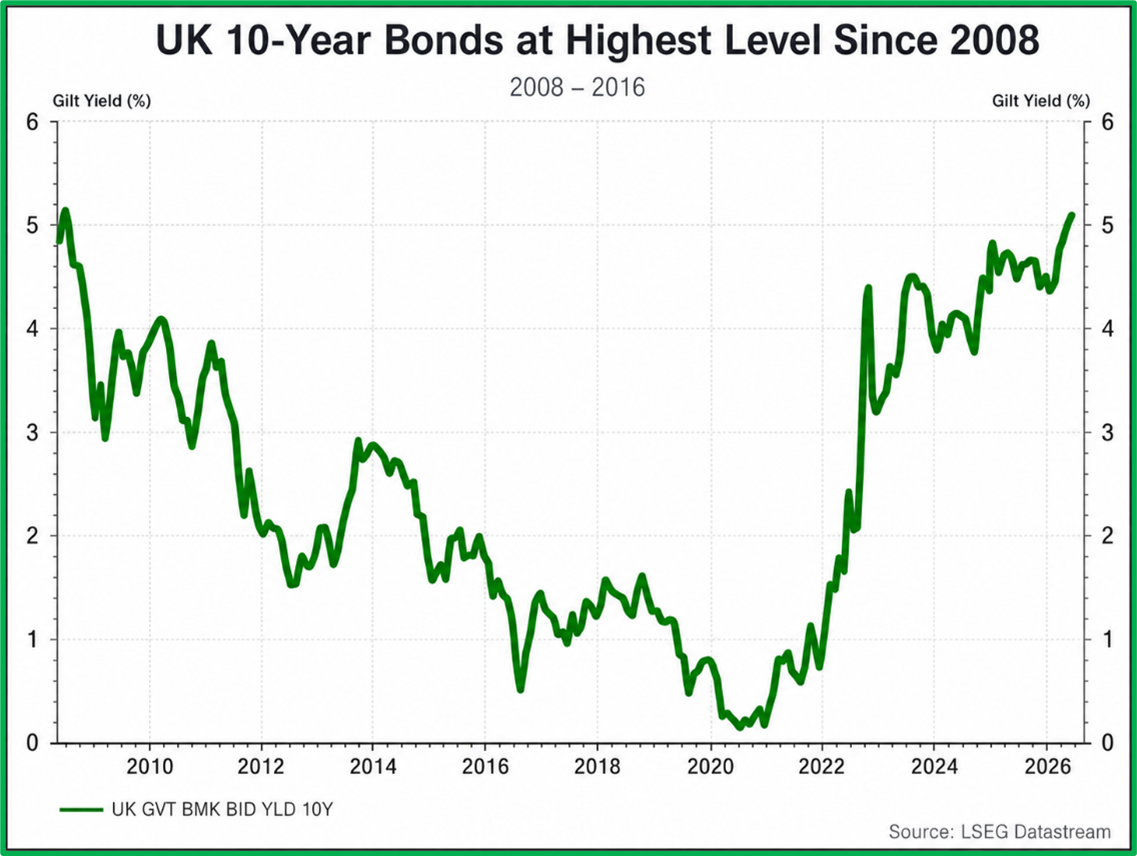

UK gilts have traditionally occupied a core role within diversified portfolios as a defensive asset – offering stability, liquidity and protection during periods of economic stress.

Lately, the combination of rising fiscal pressures, persistent inflation, elevated volatility and growing political uncertainty is increasingly challenging that assumption.

While higher yields have improved headline income potential, they also reflect materially greater risks surrounding government borrowing, inflation and debt sustainability.

In a portfolio management context, gilts now appear to offer a less attractive risk-return trade off than in prior cycles, particularly when compared with other areas of fixed income – where yields remain compelling but volatility and fiscal sensitivity may be lower.

As a result, do gilts really fulfil their traditional role as a reliable portfolio stabiliser? Are there more suitable alternatives?

UK Government Debt

At the centre of this shift is the financial position of the UK government itself.

Public debt levels remain historically elevated, while the cost of servicing that debt has increased significantly as yields have risen. Recent estimates by the Office for Budget Responsibility suggest that every 1% increase in gilt yields could add approximately £15bn annually to government debt interest costs by the end of the decade. At the same time, economic growth remains subdued, leaving policymakers with limited room for fiscal manoeuvring while increasing pressure on already stretched public finances.

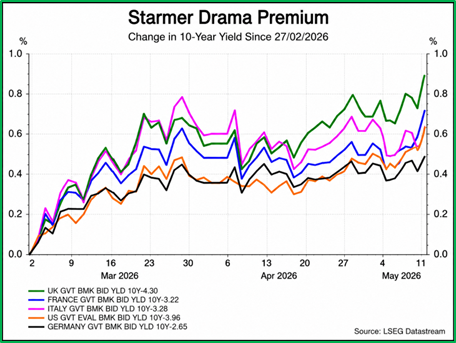

Markets have become increasingly sensitive to any signs that fiscal discipline could weaken further. Political instability has therefore become an increasingly important factor in gilt pricing.

Recent pressure surrounding Prime Minister Keir Starmer’s leadership has coincided with a rise in borrowing costs, amid concerns that a future administration may pursue looser fiscal policies and higher public spending commitments, alongside increased inflationary expectations.

These concerns have been compounded by renewed upward pressure on energy prices, which risks prolonging inflation and reinforcing expectations that interest rates may need to remain higher for longer. Bond markets tend to react quickly when confidence in fiscal credibility deteriorates, and investors are increasingly demanding additional compensation for holding UK government debt.

Is it 2022 All Over Again?

The experience of the 2022 gilt crisis also remains fresh in market memory and continues to influence sentiment towards UK government bonds.

Although market conditions today are materially different, the episode demonstrated how quickly confidence can deteriorate when concerns emerge around fiscal credibility and debt sustainability. UK gilt yields trade at a notable premium relative to many European counterparts, reflecting both domestic fiscal concerns and greater investor caution.

Politics alone, however, does not explain the rise in yields. Inflation remains a persistent concern within the UK economy, particularly given the country’s sensitivity to imported energy prices, wage pressures and weak productivity growth. Higher inflation expectations reduce the attractiveness of fixed coupon payments and require higher yields to compensate for the erosion of real returns.

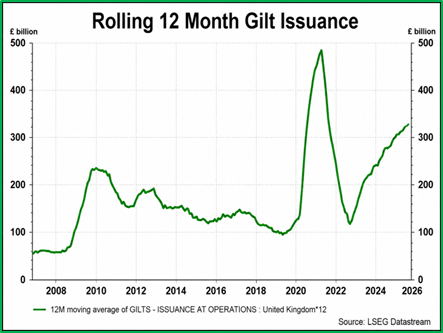

The forced buying of gilts by liability-driven investment (LDI) funds appears to have largely run its course, removing an important technical support for the UK gilt market. Following the sharp rise in gilt yields during the 2022 pension crisis, many defined benefit pension schemes were required to rebuild collateral buffers and re-establish hedging positions, leading to sustained demand for long-dated Gilts.

At the same time, the Bank of England’s quantitative tightening programme is adding further supply pressure to the gilt market. As the Bank reduces its bond holdings, the private sector must absorb a greater volume of gilt issuance at a time when government borrowing needs remain elevated (as demonstrated by Chart C showing the increase in gilt issuance). This technical backdrop has contributed to ongoing pressure across the gilt market and a steeper yield curve.

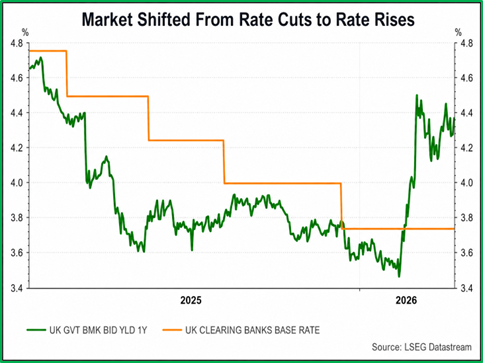

Broadly speaking, markets have undergone a significant repricing in interest rate expectations, particularly as renewed geopolitical tensions in the Middle East and the resulting spike in energy prices have intensified concerns around persistent inflation.

Investors have shifted from anticipating imminent rate cuts to recognising that rates may need to remain higher for longer, with the possibility of further tightening if inflation proves more persistent than expected. That repricing has created a difficult environment for longer-duration government bonds.

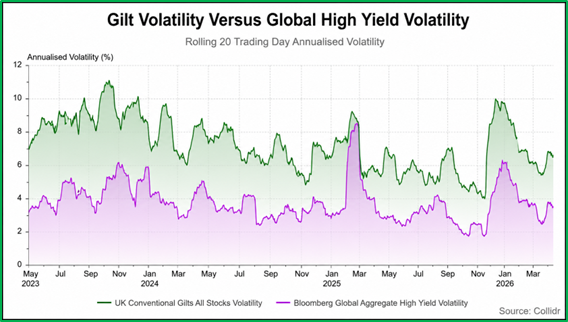

Why Volatility Matters

Volatility within the gilt market has also risen materially. In several periods over the past year, gilt market volatility has approached or exceeded levels typically associated with riskier areas of fixed income.

While current volatility levels are not unprecedented and remain below the extremes experienced during the 2022 gilt crisis, they are nevertheless indicative of a market that has become more sensitive to shifts in fiscal policy, inflation expectations and interest rate expectations. This represents an unusual development for an asset class traditionally viewed as defensive.

Higher volatility matters for portfolio construction because gilts consume more portfolio “risk budget” than they have over the longer term. This reduces their effectiveness as traditional portfolio stabilisers and reinforces the importance of active duration management and selectivity within fixed income allocations.

At Collidr, our proprietary signals remain negative on gilts due to concerns surrounding fiscal sustainability, political uncertainty, inflation risk and elevated market volatility.

While yields are now materially more attractive than they were for much of the past decade, we do not believe this alone justifies a significantly more constructive stance towards gilts within a portfolio context. Current yield levels reflect not only improved income potential, but also considerable uncertainty surrounding fiscal credibility, government borrowing requirements and the future path of inflation and monetary policy.

There also remains a meaningful risk that yields could rise further if concerns around debt sustainability persist or if inflation expectations deteriorate further. In that environment, gilts could remain vulnerable to continued volatility and shifts in investor sentiment.

The Road Forward

Looking ahead, much will depend on whether the UK government can restore confidence in the public finances while simultaneously supporting economic growth.

Greater political stability, moderating inflation and a more predictable path for Bank of England policy would all help improve conditions within the gilt market. However, while gilt yields are now materially higher than in previous years, they continue to reflect elevated fiscal, political and inflation-related risks, alongside a level of volatility that may be inconsistent with the traditional role of gilts as defensive portfolio assets.

Ongoing political uncertainty has also contributed to a more fragile market backdrop and heightened sensitivity to fiscal developments. Volatility is likely to persist in the near term, as a formal challenge to the Prime Minister could take around three months to fully resolve, depending on how the process unfolds.

In a portfolio management context, there are currently areas of fixed income offering more attractive risk-adjusted return potential, particularly where yield levels remain compelling but exposure to fiscal uncertainty and duration risk is lower.

Until there is clearer evidence of improving fiscal credibility, greater political stability and broader macroeconomic stability, caution towards gilts remains warranted, particularly for portfolios seeking reliable diversification and downside protection during periods of market stress.

For now, investing in gilts may not help you achieve what you are looking for.

Disclaimer: FOR PROFESSIONAL USE ONLY. This report was produced by Collidr Research (“Collidr”). The information contained in this report is for informational purposes only and should not be construed as a solicitation or offer, or recommendation to acquire or dispose of any investment. While Collidr uses reasonable efforts to obtain information from sources which it believes to be reliable, Collidr makes no representation that the information or opinions contained in this report are accurate, reliable or complete. The information and opinions contained in this report are provided by Collidr for professional clients only and are subject to change without notice. You must in any event conduct your own due diligence and investigations rather than relying on any of the information in the report. All figures shown are bid to bid, with income reinvested. As model returns are calculated using the oldest possible share class, based on a monthly rebalancing frequency and all income being reinvested, real portfolio performance may vary from model performance. Portfolio performance histories incorporate longest share class histories but are either removed or substituted to ensure the integrity of the performance profile is met. The value of investments and the income from them can go down as well as up and past performance is not a guide to the future performance.

Collidr Research is a trading name of Collidr Technologies Ltd, registered in England and Wales No. 09061794. Registered office: Adler House, 35 36 Eagle Street, London, WC1R 4AQ.